Among the technological responses to these challenges, asset management firms have started to adopt Artificial Intelligence, which is helping the investment teams to make better decisions and come to conviction faster.

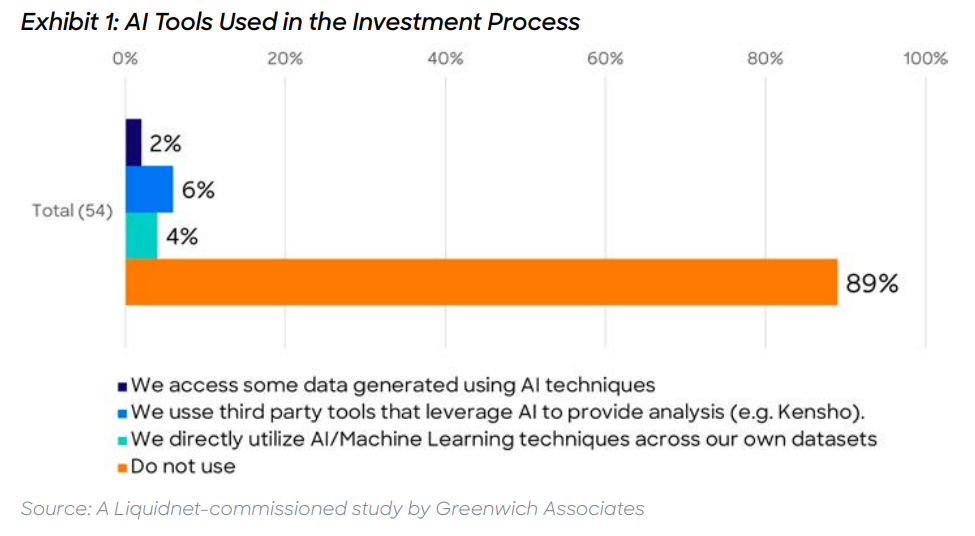

But Artificial Intelligence, like many buzzwords, is as popular as it is misunderstood. A recent Liquidnet-commissioned Greenwich Associates study indicates that only about 10% of Portfolio Managers and analysts around the world are currently using AI in the investment process. Yet, anecdotally, aren’t we hearing that EVERYONE has embraced AI by now? I wonder if a survey of those same firms’ marketing departments would show different results…

My point is that a lot of people who say they are using AI are not, and some people who are using AI don’t even know it. The latter is the more interesting case because when technology is put to its best use, we don’t know we are using it. I doubt that the folks that use 3rd party tools that leverage AI (6%), within the same Greenwich Associates study cited above, know exactly where and how AI is being deployed.

There are a few reasons why AI has not been more widely adopted. First, many alternative data providers tout their use of AI to generate a trading signal. They take unstructured content, such as written content and satellite imagery, and use various techniques to translate that raw content into structured data. AI can accelerate and improve the process because there are millions of data points (words and pixels) to train the model, and a robust training set with which to do it.

Even when the above is done well, the challenge is that the fundamental analyst doesn’t typically benefit from a data set that tries to predict price action in days or even weeks. They are called “long-term” investors for a reason. They care less about what the number of cars in the retail parking lot means for next quarter’s short-term revenue miss, and more about what the number of cars in the employee parking lot means for hiring trends.

Artificial Intelligence should be used to enable insight, and not just create data sets

Another shortfall in the use of AI is among investment research tools. According to the same Greenwich survey, alerting functionality is being used by just over half of the 56 respondents across US, Europe and APAC. The use of these alerts is for relatively simple events such as a new company filing or earnings announcement.

One use case that resonates with fundamental analysts is using Natural Language Processing (NLP) to help uncover when a company has made a notable change to some part of its filings. There is a substantial amount of academic literature in this space; the more interesting ones look at the words, phrases and changes that suggest future corporate events such M&A, litigation, or fraud. How that might translate into price movement is not necessarily a useful step.

In other words, one value proposition of Artificial Intelligence is not necessarily about predicting price, but predicting what kind of content, products, or services a user would find valuable.

Why I stopped worrying and learned to love AI

Almost everything I read or hear about on AI and automation is focused on the wrong issues. The discussion on automation versus augmentation is unhelpful; it minimises the fear of job losses by downplaying the promise of massive efficiencies. Then there is the harping on about the importance of having explanations for how a machine learns. This line of reasoning magically ignores the ignorance of our own decision-making process.

Augmentation versus automation is a false dichotomy. It would be like using quantum physics to disprove the Theory of Relativity – the two co-exist even though we don’t know how to reconcile them. Said differently, automation is necessary for any type of augmentation and, as you widen the scope of your lens, there are very few pursuits that are entirely automated.

There is no question that automation, and I am not even talking about AI, can help bring massive efficiency and additional structure to the active management process. Even the most fundamental activities can be enhanced through technology and automation, and those analysts who step up their game are the future of the industry. This is no different than the mid ‘90s where we saw rapid adoption of technology among trading firms. There are those that did, and there are those that are no more.

One of the legitimate concerns around the advancement of AI within our industry is that it favours those firms with the financial means to go hire a centralised data science team and the technology stack to support those efforts. Some large financial institutions have even begun to view technology not just as a competitive advantage, but as a weapon – something that doesn’t level the playing field, but instead obliterates it. This kind of hubris is actually encouraging. It is this hubris that will allow a disruptor to democratise these technologies and enable individuals to harness the power of Big Data and AI, levelling the playing field for people and companies alike. It’s the power of the Network.

Adam Sussman, Global head of market structure, Liquidnet