An APRA discussion paper, "Licensing: A phased approach to authorising new entrants to the banking industry", outlines a proposal for a restricted authorised deposit-taking institution (ADI) licence that will make it easier for “new entrants” such as fintechs and start-ups to enter the banking sector.

The restricted ADI licence would encourage competition within the sector and reduce barriers for new players, according to the paper.

“In particular, the purpose of the restricted ADI licence is to allow applicants to obtain a licence while still developing the full range of resources and capabilities necessary to meet the prudential framework,” the paper said.

In order to obtain the restricted licence, applicants would need to meet minimum requirements that were similar to but more relaxed than that of the ADI licence.

This would include providing APRA with details of the proposed ADI’s governance and structure, business plan model, activities, scalability, projected financials and plans to progress to the full ADI within two years.

APRA’s discussion paper also articulated that hopeful applicants would need a minimum of $3 million in start-up capital; be able to demonstrate the ADI licensee(s) were ‘fit and proper’ with the appropriate skills, experience and knowledge; and had a comprehensive, timely and credible exit plan.

Additionally, applicants would need to demonstrate reliable financial claims scheme systems and reporting, provide a description of their risk profile and proposed internal audit arrangements as well as details of their external auditor.

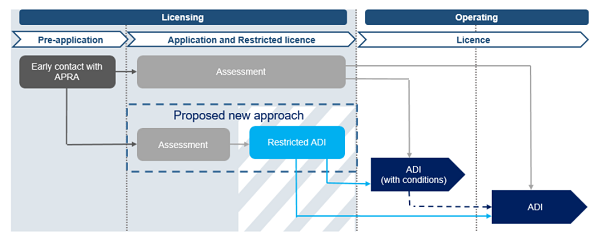

Currently, APRA’s existing licensing approach would see an applicant move from pre-application stage to assessment stage before being awarded with an ADI.

The proposed restricted licensing approach would see applicants enter a “phased approach” to obtaining a licence and move onto a restricted ADI licence for a maximum of two years, with the expectation that the licence holder would either be ready to move onto a full licence by then or exit the industry.

While the restricted ADI licence would grant applicants the opportunity to move into the banking sector earlier, it would also place certain restrictions on their banking activities to ensure the new licence would not create a competitive advantage over incumbents.

“Restricted ADIs will be strictly limited in their activity and would not be expected to actively conduct any banking business during the restricted period,” the paper states.

“Such requirements would include a limit on the maximum size of deposits from a single depositor ($250,000) and on the aggregate amount of deposits ($2 million)”.

Submissions by the public on the discussion paper will close on 30 November 2017.